Five Elements Challenging the Workforce During COVID-19

Posted on May 29th, 2020

During a recent Return to Work Alera Group webinar, nearly 500 participants were polled on the most significant challenges facing their workforce at this point in the COVID-19 crisis. Employers throughout the U.S. have had to transition their employees to remote work, or make other adjustments in their organizational structure to keep employees safe and allow the company to continue business operations.

In light of these changes, here are the top five items challenging employers across the country—and ideas on how you and your organization can proactively respond.

1. Employee Emotional Wellbeing

Rated as the top issue by 35% of employers polled, employee emotional wellbeing is hugely important. Many employees are facing challenges with remote work, including caring for children and elderly family members while trying to manage their full-time job. It is enormously difficult – and employers can respond to this stressor in a few different ways.

Employers can remind employees of an EAP (Employee Assistance Program), if it’s available, by circulating key information on how to access EAP resources. Additionally, encourage your organization’s management team to work with their employees and be cognizant of limitations brought on by remote work. Offering flexible hours or other accommodations can be extremely helpful in relieving some emotional stress for employees.

2. Employee Physical Wellbeing

Employers and employees alike are feeling the effects of physical quarantine or “shelter at home” orders. Being cooped up inside, without access to gyms or fitness studios, is impeding exercise even for highly active employees.

With this in mind, provide opportunities for employees to take care of their physical wellbeing, even during the workday. A few ideas include:

- Sharing a video to a YouTube workout that’s accessible for people with varying degrees of fitness, like this one: Lunchtime Yoga by Yoga with Adriene

- Directly encouraging employees to take a break and get up from their desk to move around

- Hire a fitness instructor to do a 30-minute Zoom session with your team to get the blood flowing

3. Employee Productivity

With a myriad of distractions coming from remote work, some employees may be struggling to remain productive during the pandemic. Employers need to recognize that this is normal and even expected, as COVID-19 impacts childcare, financial stability and other life factors for many employees.

Managers can help to mitigate productivity challenges by setting key weekly goals with their teams and checking in regularly. This, coupled with flexible hours, can help employees still reach productivity levels to maintain business functions.

During the pandemic, remote work is more prevalent than ever before—and that trend is likely to continue even post-COVID-19. While many employees find remote work to be a productive setting, there are new challenges for employers to solve for, including technology needs, restructured collaboration norms and more.

4. Employee Engagement

Along with employee productivity, employee engagement has taken a massive hit from the pandemic. 15% of those polled noted this as the most difficult factor currently facing their workforce. You can employees stay engaged through a variety of avenues:

- Working with inspirational speakers to coordinate workshop sessions on resiliency and engagement for your employees

- Clear and direct communication from your organization’s key leadership, including information on how your company is weathering the storm and how this will impact employees

- Conducting an internal survey to gauge employee engagement and current areas of organizational weakness, and then working to strengthen those areas

5. Employee Retention

Some employers are facing challenges with employee retention, particularly when partially furloughing or laying off employees. Again, clear and direct communication can be an essential part of employee retention during this time. While 401(k) matches or other benefits may be impacted by the pandemic, you can still communicate with your employees and find other opportunities to show them that they are a valued part of the organization.

Be Proactive — Create Your Engagement Plan Today!

Through all of this, it is important to be rethinking the ways your company views and engages your employee population. If you would like help rethinking and restarting your workforce during COVID-19, Alera Group’s HR Services team would love to assist. You can reach out by clicking here.

Want to learn more about this topic? Check out our webinar recording from May 13, “Rethinking and Restarting Your Workforce Amidst COVID-19".

IRS Releases 2021 HSA Contribution Limits and HDHP Deductible and Out-of-Pocket Limits

Posted on May 28th, 2020

In Rev. Proc. 2020-32, the IRS released the inflation adjusted amounts for 2020 relevant to HSAs and high deductible health plans (HDHPs). The table below summarizes those adjustments and other applicable limits.

|

|

2021 |

2020 |

Change |

|

Annual HSA Contribution Limit (employer and employee) |

Self-only: $3,600 Family: $7,200 |

Self-only: $3,550 Family: $7,100 |

Self-only: +$50 Family: +$100 |

|

HSA catch-up contributions (age 55 or older) |

$1,000 |

$1,000 |

No change |

|

Minimum Annual HDHP Deductible |

Self-only: $1,400 Family: $2,800 |

Self-only: $1,400 Family: $2,800 |

No change |

|

Maximum Out-of-Pocket for HDHP (deductibles, co-payment & other amounts except premiums) |

Self-only: $7,000 Family: $14,000 |

Self-only: $6,900 Family: $13,800 |

Self-only: +$100 Family: +$200 |

Out-of-Pocket Limits Applicable to Non-Grandfathered Plans

The ACA’s out-of-pocket limits for in-network essential health benefits have also been announced and have increased for 2021.

|

|

2021 |

2020 |

Change |

|

ACA Maximum Out-of-Pocket |

Self-only: $8,550 Family: $17,100 |

Self-only: $8,150 Family: $16,300 |

Self-only: +$400 Family: +$800 |

Note that all non-grandfathered group health plans must contain an embedded individual out-of-pocket limit within family coverage, if the family out-of-pocket limit is above $8,550 (2021 plan years) or $8,150 (2020 plan years). Exceptions to the ACA’s out-of-pocket limit rule are available for certain small group plans eligible for transition relief (referred to as “Grandmothered” plans). A one-year extension of transition relief was announced on January 31, extending the transition relief to policy years beginning on or before October 1, 2021, provided that all policies end by December 31, 2022. (This transition relief has been extended each year since the initial announcement on November 14, 2013.)

Next Steps for Employers

As employers prepare for the 2021 plan year, they should keep in mind the following rules and ensure that any plan materials and participant communications reflect the new limits:

- HDHPs cannot have an embedded family deductible that is lower than the minimum HDHP family deductible of $2,800.

- The out-of-pocket maximum for family coverage for an HDHP cannot be higher than $14,000.

- All non-grandfathered plans (whether HDHP or non-HDHP) must cap out-of-pocket spending at $8,550 for any covered person. A family plan with an out-of-pocket maximum in excess of $8,550 can satisfy this rule by embedding an individual out-of-pocket maximum in the plan that is no higher than $8,550. This means that for the 2021 plan year, an HDHP subject to the ACA out-of-pocket limit rules may have a $7,000 (self-only)/$14,000 (family) out-of-pocket limit (and be HSA-compliant) so long as there is an embedded individual out-of-pocket limit in the family tier no greater than $8,550 (so that it is also ACA-compliant).

About the Author. This alert was prepared for Alera Group by Marathas Barrow Weatherhead Lent LLP, a national law firm with recognized experts on the Affordable Care Act. Contact Stacy Barrow or Nicole Quinn-Gato at sbarrow@marbarlaw.com or nquinngato@marbarlaw.com.

The information provided in this alert is not, is not intended to be, and shall not be construed to be, either the provision of legal advice or an offer to provide legal services, nor does it necessarily reflect the opinions of the agency, our lawyers or our clients. This is not legal advice. No client-lawyer relationship between you and our lawyers is or may be created by your use of this information. Rather, the content is intended as a general overview of the subject matter covered. This agency and Marathas Barrow Weatherhead Lent LLP are not obligated to provide updates on the information presented herein. Those reading this alert are encouraged to seek direct counsel on legal questions.

© 2020 Marathas Barrow Weatherhead Lent LLP. All Rights Reserved.

Three Key Questions to Ask While Creating Your Return-to-Work Strategy

Posted on May 27th, 2020

Employers across the country are planning their strategy for returning employees to the worksite—whether that is an office building, a factory, a job site or another location. As employers develop and execute their strategic playbook, there are three key questions they should ask themselves.

1. What challenges are we trying to solve?

As a result of the crisis, some companies have seen revenue drop while other industries and businesses have seen positive or little impact on their revenue streams. The problems that each organization are working to solve are unique and that’s key to remember as you craft a return to work strategy.

Consider the specific challenges your company is trying to solve by returning to the worksite and use that as the foundation for developing your return to worksite strategy and playbook. No two playbooks will look the same!

2. What are our goals?

In the same way that your challenges will be unique to your company, your goals will also be affected by factors like your industry, size and location.

-

For some, reopening a physical office or worksite location is a crucial step to resuming business.

-

For organizations who have laid off or furloughed staff members, a goal may be to return team members to their previous working hours.

-

Many companies are concerned about meeting their 2020 budget as they feel the financial impact of COVID-19.

-

Ultimately, protecting employee and client safety should be a top priority for any company.

As you continue to navigate the new world of work with your return to worksite strategy, try implementing measurable goals that are in line with your organization’s values. One goal that is often shared is to “return to normal”—however this goal can be difficult to measure. Part of successfully restarting and rethinking the workplace may simply be “creating a sense of normalcy” and see how returning to the workplace fits into that reality.

Related: Alera Group’s Reopening a Worksite Road Map can help you work through these steps and more.

3. How will we define success?

The “global” element of this pandemic means that every company has an opportunity to respond to the crisis. Ask yourself this question: In a best-case scenario, what would “successfully navigated COVID-19” look like for your company?

You may find that innovative ideas or creative sales strategies can be key ways to measure your success. Additionally, employee health and retention are often a measure of company culture and wellbeing—and can be leveraged to evaluate the success of your return to worksite playbook.

Through all of this, it is important to be rethinking the ways your company views and engages your employee population. If you would like help developing your return to worksite strategy and playbook, Alera Group’s HR Services team would love to assist. You can reach out by clicking here.

Want to learn more about this topic? Check out our webinar recording from May 13th, “Rethinking and Restarting Your Workforce Amidst COVID-19.”

Resources for Reopening a Workplace Amid COVID-19

Posted on May 20th, 2020

With the nation in various stages of reopening from shutdowns related to COVID-19, businesses and other organizations are following procedures to keep their employees and their customers safe. Some are in the planning stages, while those that never closed are operating differently from how they did before the pandemic. Some have adapted well, while others have found themselves unprepared for reopening a workplace amid COVID-19.

Don't be unprepared. Resources are available to help you succeed. Use them.

If you're on your way to reopening, a great guide to get you there and keep you going is Alera Group's Road Map to Reopening a Worksite. The map outlines three phases:

- Strategize and Plan

- Working During COVID-19

- The New Normal

Each phase is broken into multiple steps, and each step includes considerations necessary to avoid getting tripped up.

To download, click here.

Webinars, Whitepapers and More

While the Road Map to Reopening a Worksite is a broad guide to get you through reopening and beyond, the landscape created by this coronavirus is evolving and complex. There are applications to submit; federal, state and municipal regulations to follow; and concurrencies to consider.

Navigating this landscape requires information and tools such as the Roadmap, much of which you can find in Alera Group's Coronavirus Resource Center. Content in the center includes:

|

|

|

|

|

|

|

|

|

Among the recorded webinars in the Coronavirus Resource Center is the May 13 session Restarting and Rethinking Your Workforce, which expands on the Road Map. You may also be interested in a whitepaper that examines how employers of various sizes and in different industries have responded to the economic and health crises created by the coronavirus, the COVID-19 Employer Pulse Survey.

Additional Resources for an Increasingly Online World

Alera Group clients also have access to AleraHR, an enhanced version of the ThinkHR suite of resources that includes hotline access to HR experts, webinars, an extensive library of HR materials and comprehensive online training.

AleraHR's Pandemic Response Training series launched last week with titles including:

- "General Information about Coronavirus and COVID-19"

- "Assessing Your Organization’s Risks"

- "Responding Effectively to Risks"

- "Managing in a Crisis"

- "Forging Ahead with Perseverance and Resilience"

- "Establishing Effective Virtual Teams"

- "Leading Teams: Managing Virtual Teams"

For more information about AleraHR, click here.

Guidance from a Trusted Advisor

If all that seems a bit overwhelming, I get it. Sometimes it's good just to be able to talk with a knowledgeable professional you know you can trust to look out for your best interests and provide informed advice. If you have any questions, please reach out to your Alera Group advisor or email us at info@aleragroup.com to be connected to a local firm.

About the Author

Mike Isbister

Sylvia Group, an Alera Group Company

Throughout his 30-year career in sales and service, Mike Isbister has achieved success by combining analytics and action, recognizing that having meaningful data is important — but only if you know what to do with it. The analytics-plus-action approach works not only for Mike and his team but also for Sylvia Group clients. Through the SPS process of compiling and breaking down data, they’re better able to analyze needs and exposures, review claims to determine risk-management solutions, and design comprehensive, cost-effective insurance programs.

Weekly Wrap-up: Wellbeing Resources

Posted on May 18th, 2020

We are nine weeks into this new mode of work and the pace doesn’t really seem to be slowing at all for most of you. Each week, the landscape we are living and working in seems to change dramatically, and with that comes new challenges and projects. We seem to be in a constant state of reinvention. With that said, I thought this quote I saw today from New York Times best-selling author Gabby Bernstein, aka the “Spirit Junkie”, might be useful for all of us.

‘"Solutions don’t come from pushing, they come from pausing."

Hopefully you can all find a moment to ‘pause’ this week. Have a safe and healthy week.

|

Career Wellbeing |

|

|

Social & Family Wellbeing |

Social

Family

|

|

Financial Wellbeing |

|

|

Physical Wellbeing |

|

|

Emotional Wellbeing |

|

|

Community Wellbeing |

|

|

EMPLOYER FOCUSED RESOURCES |

|

For more resources and updates, check out our Coronavirus Resource Center at aleragroup.com/coronavirus/.

About the Author

Andrea Davis, Director of Wellbeing

Andrea joined Alera Group Northeast (formerly CBP) in July 2013, bringing over 15 years of experience in management consulting and strategic solutions. As the Director of Wellbeing, she is responsible for assisting with the development, implementation and evaluation of comprehensive wellness strategies for existing and prospective Alera Group clients. She provides assistance and support to Alera Group clients by developing personalized programs that fit clients’ unique health management needs, wellness program implementation, committee development, promotion and marketing of their programs to encourage participation. In addition, Andrea conducts program analysis and generates reports related to program participation, health assessment and client utilization.

Carrier Premium Credits and ERISA Fiduciary Obligations

Posted on May 18th, 2020

Due to COVID-19 and state and local stay-at-home orders, utilization of group medical and dental insurance benefits is down. As a result, some carriers recently notified employers that they will be issued premium credits. When asking how these premium credits should be treated by the employer, we often compare then to the ACA’s medical loss ratio (MLR) rebates. While these premium credits are not MLR rebates, a similar decision must be made to determine whether they, like MLR rebates, are ERISA plan assets.

Background

As background, the Affordable Care Act’s MLR rule requires health insurers to spend a certain percentage of premium dollars on claims or activities that improve health care quality, otherwise they must provide a rebate to employers. At the same time the U.S. Department of Health and Human Services issued the MLR rule, the U.S. Department of Labor (DOL) issued Technical Release 2011-04 (TR 2011-04), which clarifies how rebates should be treated under ERISA. Under ERISA, anyone who has control over plan assets, such as the plan sponsor, has fiduciary obligations and must act accordingly.

Clearly, the premium credits we are seeing are not subject to the MLR rule; however, a similar analysis applies. TR 2011-04 clarified that insurers must provide any MLR rebates to the policyholder of an ERISA plan. However, while the DOL’s analysis was focused on MLR rebates, it recognized that distributions from carriers can take a variety of forms, such as “refunds, dividends, excess surplus distributions, and premium rebates.” Regardless of the form or how the carrier describes them, to the extent that a carrier credit, rebate, dividend, or distribution is provided to a plan governed by ERISA, then the employer must always consider whether it is a “plan asset” subject to Title I of ERISA. If it is, then as the party with authority and control over the “plan assets,” the employer is a fiduciary subject to Section 404 of ERISA and bound by the prohibited transactions provisions of Section 406. In other words, to the extent that a refund is a plan asset, it must be used for the exclusive benefit of plan participants, which may include using it to enhance plan benefits or returning it to employees in the form of a premium reduction or cash refund.

Treatment of Premium Credits to Employers

In situations where an employer uses a trust to hold the insurance policies, the DOL’s position is that the rebates are generally assets of the plan. However, in situations where the employer is the policyholder, the employer may, under certain circumstances, retain some or all of a rebate, credit, refund, or dividend. When considering whether a rebate is a plan asset, the terms of the plan should be reviewed. As discussed below, some employers draft their plan documents in a manner that allows them to retain these types of refunds. If the terms of the plan are ambiguous, the DOL recommends employers use “ordinary notions of property rights” as a guide.

When determining whether carrier credits, dividends, distributions or rebates are ERISA plan assets, the DOL will look to the terms of the documents governing the plan, including the insurance policy. If these governing documents are silent on the issue or unclear, then the DOL will take into consideration the source of funding for the insurance premium payments. In such situations, the amount of a premium credit that is not a plan asset (and that the employer may therefore retain) is generally proportional to the amount that the employer contributed to the cost of insurance coverage. For example, if an employer and its employees each pay a fixed percentage of the cost, a percentage of the premium credit equal to the percentage of participants’ cost would be attributable to participant contributions. In the event that there are multiple benefit options, a premium credit attributable to one benefit option cannot be used to benefit enrollees in another benefit option.

The Plan Document

Employers can draft their plans to make it clear that the employer retains all rebates, credits, distributions, etc. if the rebates, credits, distributions, etc. do not exceed the employer’s contribution towards the benefit. If given this flexibility in the plan, the employer may not have to return a portion of the premium credit to employees or use the credit to provide a premium reduction. While this gives employers more flexibility, employers should consider that carriers communicate some premium refunds, such as an MLR rebates, to both the policyholder and participants, therefore employees know the employer received money back from the carrier and they may expect something in return. Therefore, there is the potential for employee relations issues with this approach.

If the plan document does not provide this flexibility to the employer, is silent with regard to the use of such funds, or is unclear about how such funds are allocated, then the employer should treat any premium credits like they are ERISA plan assets (to the extent they’re attributable to employee contributions) and allocate them accordingly.

Allocating the Employees’ Share of a Premium Credit

The portion of the premium credit that is considered a plan asset must be handled according to ERISA’s general standards of fiduciary conduct. However, as long as the employer adheres to these standards, it has some discretion when allocating the premium credit.

If an ERISA plan is 100 percent employee paid, then the premium credit must be used for the benefit of employees. If the cost of the benefit is shared between the employer and participants, then the premium credit can be shared between the employer and plan participants.

There is some flexibility here. For example, if the employer finds that the cost of distributing shares of a premium credit to former participants approximates the amount of the proceeds, the employer may decide to distribute the portion of a premium credit attributable to employee contributions to current participants using a “reasonable, fair, and objective” method of allocation. Similarly, if distributing cash payments to participants is not cost-effective (for example, the payments would be de minimis amounts, or would have tax consequences for participants) the employer may apply the premium credit toward future premium payments or benefit enhancements. An employer may also vary the premium credit so that employees who paid a larger share of the premium will receive a larger share of the premium credit.

Ultimately, many employers provide the employees’ share of the premium credit in the form of a premium reduction or discount to all employees participating in the plan at the time the premium credit is distributed. Employers should review all relevant facts and circumstances when determining how such a credit will be distributed.

Regardless, to avoid ERISA’s trust requirement, the portion of a premium credit that is plan assets must be used within three months of receipt by the policyholder.

Conclusion

Employers that would like additional flexibility in how to treat carrier premium credits should work with counsel to update their plan documents. Even for plans with flexibility built into the terms, we encourage consultation with counsel to review the facts and circumstances surrounding any such premium credits to ensure compliance with ERISA.

About the Authors. This alert was prepared for Alera Group by Marathas Barrow Weatherhead Lent LLP, a national law firm with recognized experts on the Affordable Care Act. Contact Stacy Barrow or Nicole Quinn-Gato at sbarrow@marbarlaw.com or nquinngato@marbarlaw.com.

The information provided in this alert is not, is not intended to be, and shall not be construed to be, either the provision of legal advice or an offer to provide legal services, nor does it necessarily reflect the opinions of the agency, our lawyers or our clients. This is not legal advice. No client-lawyer relationship between you and our lawyers is or may be created by your use of this information. Rather, the content is intended as a general overview of the subject matter covered. This agency and Marathas Barrow Weatherhead Lent LLP are not obligated to provide updates on the information presented herein. Those reading this alert are encouraged to seek direct counsel on legal questions.

© 2020 Marathas Barrow Weatherhead Lent LLP. All Rights Reserved.

IRS Relaxes Election Change, Other Rules for Cafeteria Plans and FSAs

Posted on May 13th, 2020

As the country continues to feel the impact of the COVID-19 National Emergency declared by President Trump on March 13, 2020, the IRS has provided some much-needed guidance and relief for employees. On May 12, 2020, the IRS issued Notices 2020-29 and 2020-33, which, among other things, extend the claims period for health flexible spending arrangements (health FSAs) and dependent care assistance programs (DCAPs) and allow employees to make mid-year changes. These Notices are summarized in more detail below.

Notice 2020-29

Mid-Year Election Changes

Under Section 125 of the Internal Revenue Code, elections for qualified benefits are generally irrevocable for the plan year unless one of the permitted election change events applies. Permitted election changes allow an employee to revoke their election mid-year and make a new election on account of certain events, such as a change in status, among others.

As a result of COVID-19, some carriers offered special enrollment opportunities for employees who were otherwise eligible for the employer’s coverage, but declined coverage at open enrollment. While this may have been appreciated by employees, many employers questioned whether there was a permitted election change event under Section 125 that matched this enrollment opportunity or whether it was safer to require employees who took advantage of the opportunity to participate in the plan with after-tax contributions for the remainder of the plan year.

Additionally, many employees who previously elected to contribute to their health FSA have experienced a decrease in medical expenses as they comply with their state or local government stay-at-home orders. Therefore, they have not been able to use their health FSA contributions. The usage of DCAPs has also been disrupted due to daycare closures.

Notice 2020-29 addresses these issues for the calendar year 2020 by allowing cafeteria plans to be amended to permit employees to make mid-year election changes for the following purposes:

- For employer-sponsored health coverage:

- Make a new, prospective election if the employee had previously declined coverage;

- Revoke an existing election and make a new, prospective election to enroll in different health coverage sponsored by the employer; or

- Prospectively revoke coverage if the employee attests in writing that they are enrolled in, or immediately enroll in, other health coverage not sponsored by the employer. The Notice provides a sample attestation employers can use and may rely on the written attestation unless the employer has actual knowledge the employee is not, or will not be, enrolled in other comprehensive health coverage.

- For FSA coverage:

- Prospectively revoke an election, make a new election, or decrease or increase an election to a health FSA (including a limited-purpose health FSA) or DCAP.

Notice 2020-29 provides that employers may amend their plans to allow each eligible employee to make prospective election changes or an initial election regardless of whether the election change satisfies one of the permitted election changes under applicable Treasury regulations. The Notice is very clear that this is not a free-for-all. The employer has the discretion to impose parameters for these election changes, including the extent to which the election changes are permitted and applied, and they can limit the period during which election changes may be made.

The relief may be applied retroactively to January 1, 2020; however, as set forth above, all election changes must be prospective. The retroactive application of the relief is to cover any employer who may have allowed an election change that may not have been consistent with Section 125 (but would be consistent with one of the permitted election changes discussed above).

Finally, employers must ensure the election changes do not result in failure to comply with the nondiscrimination rules. The Notice provides strategies an employer may use to ensure there is no adverse selection of health coverage, such as limiting elections to circumstances in which an employee’s coverage will be increased or improved as a result of the election change (ex. switching from self-only to family coverage).

FSA Carryover Rules

Pursuant to Section 125, cafeteria plans may adopt a carryover, which allows participants to carry over unused amounts remaining at the end of the plan year. The carryover allows the plan to reimburse participants for medical care expenses incurred during the following plan year (up to $550 – see the discussion of Notice 2020-33 below). Alternatively, a plan may adopt a grace period, which gives plan participants up to an additional two and one-half months to apply any unused funds remaining in the health FSA or DCAP at the end of the plan year. The plan may adopt either carryover or the grace period (not both), or the plan can choose not to offer either option.

Because the COVID-19 National Emergency will likely result in employees having unused health FSA or DCAP contributions at the end of the plan year, Notice 2020-29 allows an employer to amend its plan to permit employees to apply any unused amounts in a health FSA or DCAP at the end of a plan year ending in 2020 (or grace period ending in 2020, if applicable) to pay or reimburse medical care expenses or dependent care expenses, respectively, incurred for the same qualified benefit through December 31, 2020. Even plans with a carryover may adopt this grace period (despite the prohibition on having both a carryover and a grace period).

This extension applies to all health FSAs (including limited purposes FSAs) and, if adopted, may potentially impact an employee’s eligibility to contribute to an HSA (unless the health FSA is a limited-purpose health FSA) during the extended period.

This relief can be applied on or after January 1, 2020 and on or before December 31, 2020 provided any elections made pursuant to the relief are made only on a prospective basis.

High Deductible Health Plans

COVID-19 testing and treatment

Under current law, with limited exceptions, a high deductible health plan (HDHP) will fail to be HSA-qualified if it allows certain medical care services or items to be purchased prior to meeting the applicable minimum deductible.

Notice 2020-15, issued by the IRS in March, provided that an HDHP would not fail to meet its qualified status simply by allowing participants to receive testing and treatment of COVID-19 without having to meet the minimum deductible.

Notice 2020-29 clarifies that this applies with respect to reimbursements incurred on or after January 1, 2020, and that the panel of diagnostic testing for influenza A & B, norovirus and other coronaviruses, and respiratory syncytial virus (RSV) and any items and services required to be covered with zero cost-sharing pursuant to the FFCRA, as amended by the CARES Act, are covered pursuant to Notice 2020-15.

Telemedicine

Similarly, for purposes of the temporary safe harbor (through plan years beginning on or before December 31, 2021) for a qualified HDHP to provide coverage for telehealth and other remote care services at no cost to employees without disrupting HSA eligibility, Notice 2020-29 provides that this will apply for purposes of services provided on or after January 1, 2020, with respect to plan years beginning on or before December 31, 2021.

Employers have until December 31, 2021 to adopt any of the plan amendments described in Notices 2020-29 and 2020-33 and the plan amendment may apply retroactively to January 1, 2020; however, employers must inform their employees eligible to participate in the plan of these changes.

Notice 2020-33

Health FSA Carryover Limit

Notice 2020-33 modifies prior guidance by indexing the health FSA carryover limit ($500) for inflation consistent with the indexed limit for the health FSA contribution limit for 2020. Therefore, the health FSA carryover limit increases by 20%, from $500 to $550 effective January 1, 2020.

If a cafeteria plan chooses to increase the carryover limit to $550, it must notify all individuals eligible to participate in the plan of this change and will have until December 31, 2021 to adopt a plan amendment.

Individual Coverage HRAs (ICHRAs)

Individual coverage health reimbursement arrangements (ICHRAs) are HRAs an employer may adopt under certain circumstances to allow employees to reimburse premiums for individual health insurance (or Medicare premiums) and other medical care expenses if certain circumstances are satisfied. An ICHRA is an employer-sponsored health plan and reimbursements for medical expenses incurred by a participating employee during the plan year are excluded from the employee’s gross income.

The limitation on the ICHRA to reimburse only those medical care expenses incurred within the plan year creates an administrative issue when participants must pay their premiums before the first day of the plan year. To overcome this administrative issue, Notice 2020-33 allows an ICHRA to treat an expense for a premium for health insurance coverage as incurred on:

- the first day of each month of coverage on a pro-rata basis

- the first day of the period of coverage, or

- the date the premium is paid.

Employers who would like to avail themselves of the relief provided in the Notices should work with their ERISA attorney, insurance broker or cafeteria plan vendor to ensure the plan is amended to reflect any conditions or limitations the employer may apply.

————————————————————————————————————————-

The information provided in this alert is not, is not intended to be, and shall not be construed to be, either the provision of legal advice or an offer to provide legal services, nor does it necessarily reflect the opinions of the agency, our lawyers or our clients. This is not legal advice. No client-lawyer relationship between you and our lawyers is or may be created by your use of this information. Rather, the content is intended as a general overview of the subject matter covered. This agency and Marathas Barrow Weatherhead Lent LLP are not obligated to provide updates on the information presented herein. Those reading this alert are encouraged to seek direct counsel on legal questions.© 2020 Marathas Barrow Weatherhead Lent LLP. All Rights Reserved.

Weekly Wrap-up: Wellbeing Resources

Posted on May 11th, 2020

We have all felt the mental health impacts from this crisis and so many of you have done an amazing job making this a focus in the programming you are bringing to employees during this time.

A study published this week paints an even bleaker picture than I imagined. More than 1 in 4 American adults met the criteria that psychologists use to diagnose serious mental distress and illness, a 700% increase from pre-pandemic data. Young adults and those with children experienced the most pronounced increases. In adults living at home with kids under the age of 18, the rate of severe distress rose from 3% in 2018 to 37% last month. Full data is shared in the employer resources section below.

As you continue to work through the unique challenges that are facing your employees during this time, please let us know how we can support you. Have a safe and healthy week.

|

Career Wellbeing |

|

|

Social & Family Wellbeing |

Social

Family

|

|

Financial Wellbeing |

|

|

Physical Wellbeing |

|

|

Emotional Wellbeing |

|

|

Community Wellbeing |

|

|

|

|

|

EMPLOYER FOCUSED RESOURCES |

|

About the Author

Andrea Davis, Director of Wellbeing

Andrea joined Alera Group Northeast (formerly CBP) in July 2013, bringing over 15 years of experience in management consulting and strategic solutions. As the Director of Wellbeing, she is responsible for assisting with the development, implementation and evaluation of comprehensive wellness strategies for existing and prospective Alera Group clients. She provides assistance and support to Alera Group clients by developing personalized programs that fit clients’ unique health management needs, wellness program implementation, committee development, promotion and marketing of their programs to encourage participation. In addition, Andrea conducts program analysis and generates reports related to program participation, health assessment and client utilization.

Employer Insurance Premium Payment Grace Periods & Premiums Returned to Employers Inadvertent ERISA Issues

Posted on May 11th, 2020

During this pandemic, many employers are having to curtail operations and are going through the difficult process of finding cost-saving measures because of the sudden reduction in revenue caused by the various COVID-19 related state and local government orders.

Many carriers are allowing, and some states are requiring insurance policies to remain in force even if premiums are not paid timely. In addition, some fully insured carriers, knowing employees have not been able to utilize their insurance due to non-emergency services being closed (e.g. dental exam), may be returning premiums paid to employers or giving a reduction in the monthly premium as a good faith gesture.

This payment grace period and refund of premiums may be a welcome relief to employers who are finding it challenging to meet their financial obligations. However, employers, should be aware of possible consequences before taking advantage of these carrier grace periods and also understand how they may utilize the premiums returned to them, if their plans are subject to ERISA (i.e. virtually all private-sector employers who establish or maintain a welfare benefit plan, fund or program for their employees).

Background – ERISA’s Fundamental Fiduciary Rules

ERISA sets minimum standards and requirements for welfare benefit plans (e.g. group health plan) including how plan assets must be handled by those administering or managing the plan (i.e. fiduciary responsibilities). Anyone who exercises any discretionary authority or control over a plan; exercises any authority or control over a plan’s assets; has any discretionary authority in administering a plan is deemed to function as a fiduciary under ERISA, even if not named as a fiduciary in the plan’s governing documents.

Fiduciaries have important responsibilities and are subject to standards of conduct because they act on behalf of group health plan participants and their beneficiaries. These responsibilities include:

- solely in the interest of plan participants and their beneficiaries and with the exclusive purpose of providing benefits to them;

- out their duties prudently;

- the plan documents (unless inconsistent with ERISA);

- plan assets (if the plan has any) in trust; and

- only reasonable plan expenses.

How Do These Responsibilities Affect the Operation of the Plan?

EMPLOYEE CONTRIBUTIONS

If a plan provides for salary reductions from employees’ paychecks for contribution to the plan or participants pay directly, such as the payment of COBRA premiums, then the employer must make plan insurance premium payments or deposit the contributions in a plan trust, in a timely manner.

The law requires that participant contributions (i.e. plan assets) be deposited in the plan as soon as it is reasonably possible to segregate them from the company’s assets, but no later than 90 days from the date when the employer withholds or receives them. If employers can reasonably deposit the contributions sooner, they must do so. For plans with fewer than 100 participants, salary reduction contributions deposited with the plan no later than the 7th business day following withholding by the employer will be considered contributed in compliance with the law.

For participant contributions to cafeteria plans (also referred to as Internal Revenue Code Section 125 plans), the Department will not assert a violation solely because participant contributions were not held in trust.

Other contributory health plan arrangements may get the same relief if the participant contributions are used to pay insurance premiums within 90 days of receipt.

If an employer withholds employee salary reductions but does not use the funds in a timely manner or misuses the funds (e.g. paying rent) this may be considered a “prohibited transaction” (i.e. what not to do with the Plan’s assets) and breach of fiduciary duty.

INSURANCE COMPANY REFUNDS

Distributions from insurance companies to employers for their employee benefit plans, take a variety of forms, including refunds, dividends, demutualization payments, rebates, and excess surplus distributions. To the extent that these distributions are considered to be plan assets, they become subject to fiduciary responsibility and prohibited transaction provisions of ERISA.

ERISA does not expressly define plan assets, however, there are regulations describing what constitutes plan assets with respect to participant contributions. In general, the portion of a refund that is attributable to participant contributions would be considered plan assets. Thus, if the employer paid the entire cost of the insurance coverage, then no part of the refund with respect to this particular policy would be attributable to participant contributions. However, if participants paid the entire cost of the insurance coverage, then the entire amount of the refund would be attributable to participant contributions and considered to be plan assets. If the participants and the employer each paid a fixed percentage of the cost, a percentage of the refund equal to the percentage of the cost paid by participants would be attributable to participant contributions. There are also rules on what may be done with plan assets to ensure they are used for the exclusive benefit of plan participants and beneficiaries.

Examples:

AL Machine Shop offers Chopper Insurance dental plan to its full-time employees. The employees who elect coverage pay 100% the cost of coverage pretax via their S.125 plan. There are 100 employees enrolled in dental coverage. Chopper Insurance returned $1,000 of premium to AL Machine Shop due to employees not able to use their plan for two months. The employees contributed 100% of the premium, so 100% of the rebate would need to be used for the benefit of the employees. AL Machine Shop could decide to reduce each enrolled employee’s pretax contribution to the next pay period by $10.

Peanut’s Candy Store offers Ojo Insurance vision plan to its full-time employees. The employees who elect coverage contribute 50% of the premium on a post-tax basis. There are 15 employees enrolled in vision coverage. Ojo Insurance returned $750 of premium to Peanut’s Candy Store due to employees not able to use their plan for three months. 50% of $750 or $375 would need to be used for the benefit of plan participants. Peanut’s Candy Store could decide to provide a $25 refund to each employee via their next paycheck. The refund is a return of contributions originally withheld from the employee’s paycheck on a post-tax basis, therefore the refund provided to employees generally will not be subject to income taxes.

Due to lack of utilization during the pandemic, an insurance carrier may voluntarily return premiums to an employer. A portion or all of this refund may be considered a plan’s assets and how the refund is used may have restrictions.

Determining whether any part of the refund is a plan's asset, is based on factors such as the terms of the plan document and whether employees paid any portion of the premiums. If any part of the refund is a plan asset, the employer must decide, consistent with ERISA’s fiduciary rules, how to allocate the refund, such as distributing to participants, enhancing plan benefits or reducing future participant premiums. Guidance suggests this allocation must occur within three months of receipt, or the plan assets must be held in a trust.

Employers should keep in mind, when refunding premiums to employees the tax consequences depending on whether the salary reductions were made on a pre-tax basis through a Section 125 plan, or post-tax. If salary reductions were pretax, the refund generally will be taxable income subject to employment taxes.

CONSEQUENCES OF FAILURE TO FULFILL FIDUCIARY DUTIES

- liability to make plan whole –restore plan losses

- & IRS may assess civil penalties

- may be removed and barred from being a fiduciary

Note: Any person who is a decision-maker regarding a Plan, is an ERISA fiduciary. ERISA has a “functional” definition – it is not dependent on job title or documents. Many fiduciaries fail to understand that they can be held personally liable for a breach of fiduciary duty, even when the breach is unintentional.

Possible ERISA Consequences of Taking Advantage of a Carrier Grace Period

If the employer is delaying payment of the carrier invoice but due to unforeseen business circumstances is unable to catch up (e.g. bankruptcy) and the carrier due to nonpayment of premium, ends up canceling the insurance plan retroactively, any employee who saw a health care provider during the grace period may find themselves faced with denied claims, or receive bills from providers for health care visits previously paid which the carrier is recouping. Likewise, other benefits an employee thought they had available to them, (e.g. life insurance) an employee or beneficiary may discover that plan too was canceled and benefits not available. Consequently, an employee, dependent or beneficiary may sue if they were improperly denied benefits, coverage or reimbursement.

In addition to the plan fiduciary possibly being personally liable for the claims, they also may have additional consequences if during investigations into the plan’s activities by the Department of Labor it was discovered that employee’s salary reductions were never used for their intended purpose.

Possible ERISA & IRS Consequences of Improperly Using Carrier Refunds

There is no de minimis exception to ERISA's fiduciary rules for the use of plan assets. Nor is it permissible to use plan assets to pay for expenses that are for the benefit of the employer, (e.g. tax consulting fees). An employer, upon audit, may have to substantiate how they determined which portion of the carrier refund was a plan asset and how these assets were allocated. Or participants, upon learning about a refund, may inquire about the status and sue for breach of fiduciary duties.

Self-Funded Or Level-Funded Plan Considerations

If employers receive a surplus or refund, the terms of the plan should be reviewed before deciding a course of action. Any amounts that are attributable to participant contributions are plan assets. However, many plan documents will include plan language indicating that participant contributions are used to pay claims prior to using employer funds, therefore it is possible any surplus, refunds or other adjustments in fees belong to the employer. Employers who have based participant contributions off of maximum total costs and find themselves with lower expected costs, may want to consider reflecting the low utilization in their 2021 calculations.

Communication with Employees

If an employer has decided they will not be returning a portion of the refund directly to employees, they may want to consider proactively communicating with employees how they intend to use the plan asset portion of the refund for the employee’s benefit. This may help alleviate employee relations issues arising if employees learn about carriers providing refunds to employers.

Employer Options to Consider for Reducing ERISA Risks

A critical consideration is the viability of the business long term if the COVID-19 state of emergency continues and the employer’s ability to pay back the premiums owed in the future. If the possibility exists the employer may not be able to pay their debt, the employer should consider canceling the insurance coverage and providing honest and accurate information to employees about their benefits. If salary reductions have occurred that were not sent to the carrier, these should be returned to the employee. If carriers have provided a refund, employers may want to consider providing the employee’s share of the refund in the form of a future premium reduction, or cash (subject to appropriate tax treatment.) If a carrier provides a reduction in the monthly premium for a plan which is 100% paid by employee salary reductions (e.g. no employer contribution), employers should reduce the employees’ salary deduction accordingly.

Employers that wish to take advantage of the carrier’s grace period or receive a refund, to avoid missteps that could result in legal or tax liability, as well as mitigate any disastrous impact on their employees, should consult with their legal counsel to fully understand the administrative, tax or legal impediments to any contemplated action.

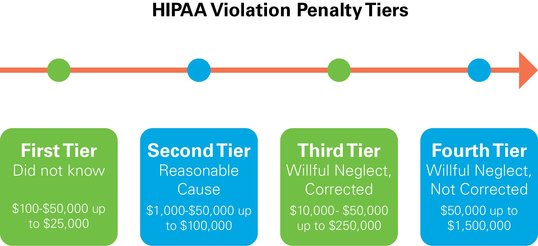

Being Prepared for a HIPAA Audit

Posted on May 4th, 2020

The Office of Civil Rights (OCR) periodically audits covered entities (i.e. health plans, health care clearinghouses, and health care providers) to ensure compliance with HIPAA’s regulations. HIPAA audit or investigation penalties for noncompliance can amount to millions of dollars depending on the level of negligence. Although, HIPAA regulations are overwhelming to many, OCR does provide its audit protocol which can be used as a guideline to assess the potential areas OCR may look for during an audit and includes information on what HIPAA regulations require for compliance. Group health plan sponsors should use OCR’s audit protocol as a guide & take steps to prepare themselves.

STEPS TO COMPLIANCE:

1. Designate & train (different roles but may be the same individual for all three functions):

- a. HIPAA privacy office

- b. A contact person for receiving complaints & answering employee questions

- c. A HIPAA security officer (technology)

2. Identify areas of risk through an assessment – e.g. identify and review how the group health plan uses and discloses PHI, what individuals or departments have access, how is PHI access limited, assess vulnerability to where electronic PHI is stored; received,

maintained or transmitted

3. Develop written policies & procedures* implementing appropriate administrative and safeguards to protect the privacy of PHI

4. Roll-out the program & document training to all participants of its workforce with access to PHI

5. Re-evaluate program annually

*Examples of written policies & procedures needed include but are not limited to:

- Procedures to reasonably ensure only the minimum necessary PHI to complete a task and only those who need PHI to perform their functions for the group health plan have access to the information.

- Procedure to distribute HIPAA Notice of Privacy Practices reminder to participants enrolled in the group health plan and at a minimum every 3 years

- Procedure to identify current and future business associates and ensure Business Associate Agreement (BAA) is in place

- Process to allow employees to inspect, receive a copy, request amendments to or restrict uses and disclosures of their PHI

- Complaint procedures if the employee believes their privacy rights have been violated

- Procedure to mitigate risk if a violation of HIPAA policies & procedures occurs and consequences to an employee who used or disclosed PHI inappropriately

HIPAA requires covered entities and persons or entities who create, receive or maintain protected health information (PHI) on behalf of a covered entity (i.e. business associates) to implement privacy and security policies and procedures to protect individually identifiable health information.

A covered entity at a minimum should review its policies when changes are made to HIPAA regulations when business processes change, different technology implemented, or new state laws are passed. It’s also imperative for an organization to review its policies if they experience a data breach or security violation and HIPAA requires a risk assessment be performed. Failure to perform an assessment may be considered “willful neglect”, which is subject to the highest monetary fines.

The best way to prevent a breach or come away from a HIPAA audit successfully is for covered entities to understand the privacy and security rules defined by HIPAA, demonstrate compliance and comply with HIPAA’s regulations.

Disclaimer: This blog was written by Michelle Turner, MBA, Compliance Consultant, Alera Group Central Region. This blog post intends to provide general information regarding the status of, and/or potential concerns related to, current employer HR & benefits issues. This blog should not be construed as, nor is it intended to provide, legal advice. The opinions expressed herein are based upon the author’s experience as a Compliance Consultant and may not reflect the opinions of your counsel.

Current as of 5/4/20

The information contained herein should be understood to be general insurance brokerage information only and does not constitute advice for any particular situation or fact pattern and cannot be relied upon as such. Statements concerning financial, regulatory or legal matters are based on general observations as an insurance broker and may not be relied upon as financial, regulatory or legal advice. This document is owned by Alera Group, Inc., and its contents may not be reproduced, in whole or in part, without the written permission of Alera Group, Inc.